late <- fixest::feols(Y ~ 1 | D ~ Z, data = mydata, se = "hetero")Quasi-Experimental Methods

In the chapter 5, we introduced the frameworks of causal inference, and how randomisation can establish causality.

However, in the social sciences, we cannot always run randomised experiments where we control the assignment of treatment. In fact, in most scenarios, we have to rely on observational data. In this chapter, we introduce methods to identify causal effects when randomisation is not possible.

Overview

In chapter 5, we discussed how randomised experiments can establish causality. However, in the social sciences, randomised experiments where researchers control treatment assignment are not always possible to implement. Sometimes even with randomisation, something goes wrong, and we need another way to establish causality.

As a result, a series of quasi-experimental designs have been developed in order to estimate causal effects. These designs range in terms of credibility, and can generally only be implemented in certain scenarios where the real-world aligns with the specific design. The main designs, in order of credibility, are:

| Design | When to Use | Estimands |

|---|---|---|

| Non-Compliance Designs | When we have a randomised experiment, but some individuals do not comply with the treatment we assigned with them. | LATE, ITT |

| Regression Discontinuity | When treatment is assigned in the real-world by some cut-off value of some variable. | LATE |

| Examiner Instruments | When treatment assignment is influenced by the quasi-random assignment of individuals to decision makers (examiners), such as judges, doctors, caseworkers, etc. | LATE |

| Shift-Share Instruments | When treatment is assigned based on some exposure (share) to some exogenous/random shock (shift). | LATE |

| Differences-in-Differences | When there is variation in time of implementation of treatments between areas/units. | ATT |

| Selection on Observables | When treatment is believed to be assigned based on a set of variables (covariates) that we can observe. | ATE, ATT |

We will explore each of these designs in more details below.

Non-Compliance Designs

When we assign individuals to treatment/control in randomised experiments, we often cannot guarantee that individuals will actually follow through with treatment. Let us assume an encouragement \(Z_t \in \{0, 1\}\), which is our treatment assignment. Then, we have the treatment variable \(D_t \in \{0,1\}\), which is someone who actually took the treatment or not. Given this framework, we can divide all units \(i\) into 4 categories:

- Compliers: People who comply with encouragement \(Z_i\). Their \(Z_i = D_i\).

- Always-takers: People who no matter what encouragement \(Z_i\) is, always take treatment.

- Never-takers: People who no matter their encouragement \(Z_i\) is, never take treatment.

- Defiers: People who do the opposite of encouragement \(Z_i\), so always \(D_i ≠ Z_i\).

Principle Strata

We can visually show what will happen with all 4 types of people in a table, called the principal strata:

| \(Z_i = 1\) | \(Z_i = 0\) | |

| \(D_i = 1\) | Complier/Always-Taker | Defier/Always-Taker |

| \(D_i = 0\) | Defier/Never-Taker | Complier/Never-Taker |

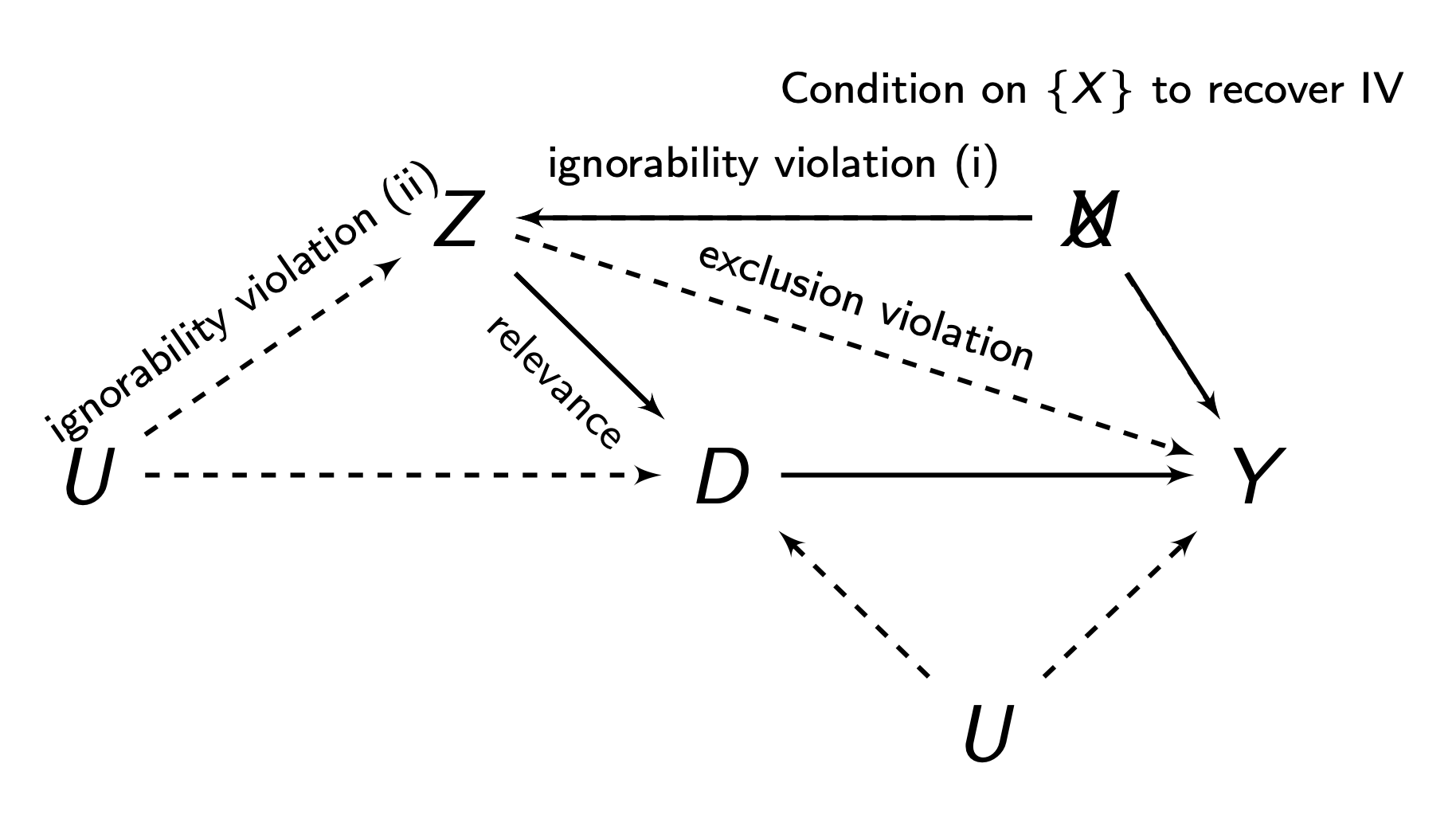

The idea of the non-compliance designs is to use our encouragement/treatment assignment \(Z\) as an instrument for \(D\) - actually taking the treatment.

There are 4 assumptions to the non-compliance designs:

- Relevance: \(Z\) must be correlated to \(D\), i.e. \(Cov(Z,D)≠0\). Or in other words, compilers must exist, or else, encouragement \(Z\) would not affect treatment \(D\).

- Ignorability/Exogneity: There is no backdoor path between \(Z\) and \(D\), and no backdoor path between \(Z\) and \(Y\) (we can do controls/selection on observables to account for this). This is generally met if our \(Z\) in our non-compliance design is randomly assigned.

- Exclusions Restriction: \(Z\) must only have an effect on \(Y\) through \(D\). \(Z\) must not have any independent effect on \(Y\).

- Monotonicity: There are no defiers - people who do the opposite of their encouragement \(Z\), no matter what \(Z\) they get.

We have two estimands of interest. The Intent to Treat (ITT) is the ATE of \(Z\) on \(Y\). This is the effect of encouragement:

\[ \tau_{ITT} = \E(Y_t|Z_t = 1) - \E(Y_t | Z_t = 0) \]

However, the ITT does not tell us anything about the effect of \(D\) (the treatment), only \(Z\) (the encouragement). The Local Average Treamtment Effect (LATE) provides the effect of the treatment \(D\) on \(Y\) for compliers (so the ITT or ATE for compliers):

\[ \tau_{LATE} = \E(\tau_t | \mathrm{compliers}) \]

The LATE is generally not equivalent to the ATT or the ATE.

The ITT itself is identifiable under exogeneity/ignorability alone, since \(Z\) is randomly assigned in non-compliance designs.

To identify the LATE, we will need all 4 assumptions. Let us define \(c\) as compliers, \(a\) as always-takers, \(n\) as never-takers, and \(d\) as defiers. We can break down the ITT into a weighted average:

\[ \tau_{ITT} = \tau_{ITT}^c \P(c) + \tau_{ITT}^a \P(a) + \tau_{ITT}^n \P(n) + \tau_{ITT}^d \P(d) \]

We know that under our assumption of monotonicity, we assume no defiers, so the probability of a defier is \(\P(d) = 0\):

\[ \tau_{ITT} = \tau_{ITT}^c \P(c) + \tau_{ITT}^a \P(a) + \tau_{ITT}^n \P(n) \]

Our exclusions restriction says that \(Z\) has no independent effect on \(Y\). The ITT is the relationship between \(Z\) and \(Y\). But since always-takers and never-takers ignore \(Z\) when deciding treatment, \(Z\) has no effect of them on \(Y\). Thus, we can further simplify:

\[ \tau_{ITT} = \tau_{ITT}^c \P(c) \]

Remember that the \(\tau_{ITT}\) for compliers, \(\tau_{ITT}^c = \tau_{ATE}\). So, let us isolate it to get:

\[ \tau_{LATE} = \frac{\tau_{ITT}}{\P(c)} \ = \ \frac{\E(Y_i | Z_i = 1) - \E(Y_i | Z_i = 0)}{\E(D_i | Z_i = 1) - \E(D_i | Z_i = 0)} \]

For estimation, we could our sample equivalents in. Alternatively, we can use 2SLS (shown below), which produces equivalent estimates.

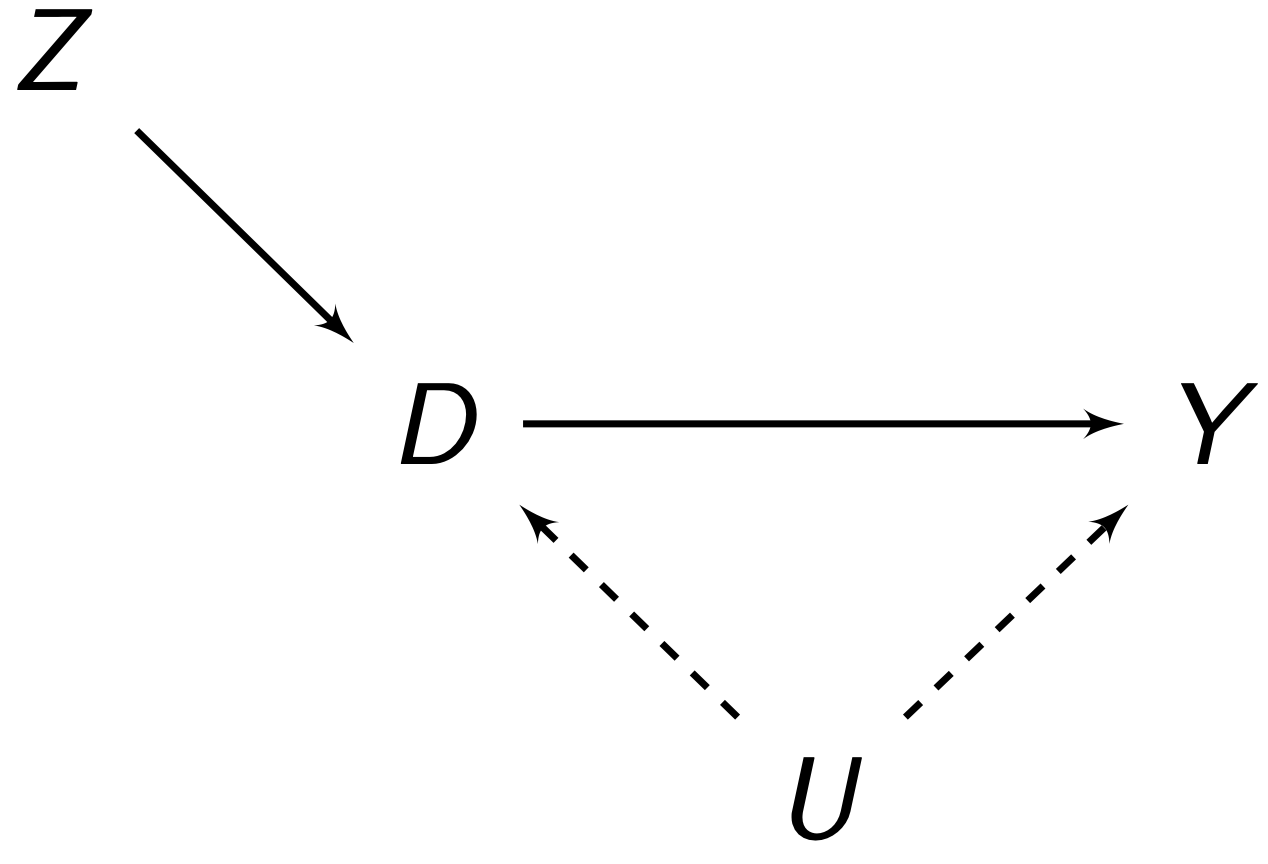

The typical \(Z\) setup in instrumental variables (and the non-compliance design) is:

Since we use only the compliers (the part of \(D\) that is explained by \(Z\)) for the LATE, \(Z\) determines \(D\), and not \(U\). Thus, we have broken the link \(U \rightarrow D\), thus eliminating our confounder problem. The weaknesses of the design are the numerous possible violations:

In a non-compliance design, since \(Z\) is randomly assigned, ignorability is generally not a huge concern. Relevance is generally met assuming we have compliers. Our main concern is the exclusions restriction.

To estimate the LATE in a non-compliance design, we typically use the 2-stage least squares estimator, as was detailed previously.

The 2SLS estimator (and IV estimator) are biased in small sample sizes, but asymptotically consistent, so we should be more careful when dealing with small samples.

When interpreting the LATE, we must be careful. The LATE is only the causal effect of taking the treatment for compliers. However, we cannot say anything about non-compliers, and we must be careful about generalising. We generally do not know who the compliers are as well, and different \(Z\) can result in different compliers.

Regression Discontinuity

Regression discontinuity designs are used when treatment is assigned based on some cutoff. For example, perhaps students only get scholarships if they get a certain score or above, or people get something after a certain age.

We have some treatment \(D_t\). There is some forcing variable \(X_t\) that perfectly determines \(D_t\) at some cutoff point \(X_t = c\).

\[ D_t = \begin{cases} 1 & \text{if } X_t > c \\ 0 & \text{if } X_t ≤ c \end{cases} \]

The idea is that right below and above the cutoff, individuals \(t\) are very similar. Thus, we have quasi-random variation and comparable treatment-control groups at the cutoff which we can use to find the treatment effect at the cutoff point.

There are 2 main assumptions for sharp regression discontinuity:

- Continuity: the potential outcomes \(\pt\) and \(\pc\)’s averages are continuous at cutoff \(X_t = c\). There can be no breaks or jumps in potential outcomes:

\[ \begin{align} & \lim\limits_{\epsilon \rightarrow 0} \E (\pt | X_t = c + \epsilon) = \E (\pt | X_t = c) \\ & \lim\limits_{\epsilon \rightarrow 0} \E (\pc | X_t = c + \epsilon) = \E (\pc | X_t = c) \\ \end{align} \]

- Perfect Compliance: The cutoff \(X_t = c\) perfectly decides who gets the treatment and who does not get the treatment.

Our estimand is the Local Average Treatment Effect (LATE) at the cutoff point \(X_t = c\):

\[ \tau_{LATE} = \E(\pt - \pc | X_t = c) \]

We can identify the LATE with the continuity assumption. We start with the LATE:

\[ \tau_{LATE} = \E(\pt | X_t = c) - \E(\pc | X_t = c) \]

And using the assumption of continuity, we can substitute the expectations at \(X_t = c\) with limits. We also know that if a limit exists, then both one-sided limits must be equal:

\[ \begin{align} \tau_{LATE} & = \lim\limits_{\epsilon \rightarrow 0} \E (\pt | X_t = c + \epsilon) - \lim\limits_{\epsilon \rightarrow 0} \E (\pc | X_t = c + \epsilon) \\ & = \lim\limits_{\epsilon \rightarrow 0^+} \E (\pt | X_t = c + \epsilon) - \lim\limits_{\epsilon \rightarrow 0^-} \E (\pc | X_t = c + \epsilon) \end{align} \]

And we know we that individuals above the cutoff are assigned to treatment, and individuals below are assigned to control, so we can observe both of the above terms, and get:

\[ \tau_{LATE} = \lim\limits_{\epsilon \rightarrow 0^+} \E (Y_t | X_t = c + \epsilon) - \lim\limits_{\epsilon \rightarrow 0^-} \E (Y_t | X_t = c + \epsilon) \]

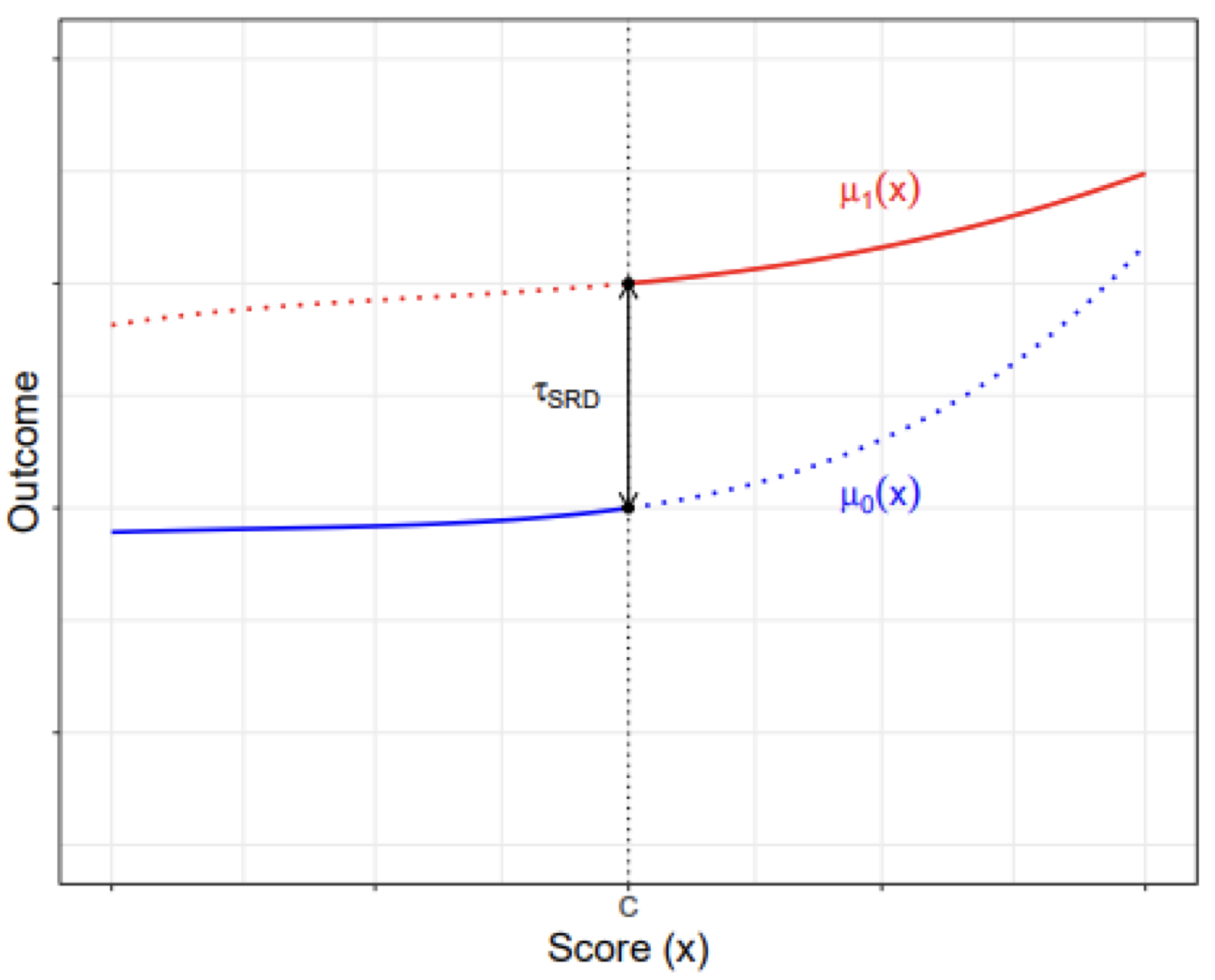

The idea of regression discontinuity is shown below. The Red is the potential outcomes \(\pt\), and the red is the potential outcomes \(\pc\).

Any difference in observed outcomes at the cutoff \(X_t = c\) should be the treatment effect \(\tau_{LATE}\) at the cutoff.

To estimate a regression discontinuity, we model of potential outcomes \(\pt\) and \(\pc\), and find the “discontinuity” at the cutoff.

The current “state of the art” RDD is to assume \(\pt\) and \(\pc\) are nonparametric (no functional form), and use a non-linear method to model them.

First, We need to recenter our forcing variable \(X_t\) so that the cutoff \(c = 0\).

my_data$X <- my_data$X - cThen, we should filter our data such that only observations within our bandwidth are included (so observations between \(c - h ≤ X_t ≤ c + h\)). Selecting a bandwidth will be discussed in the next tab:

library(tidyverse)

my_data <- mydata %>%

select(X <= h) %>%

select(X >= -h)Then, we can estimate the LATE with the rdrobust package:

We need to make 3 choices when fitting nonparametric models: polynomial \(p\), kernel \(K(\cdot)\), and bandwidth \(h\).

- \(p\) is the flexibility of the model. We generally just use \(p = 1\).

- \(K(\cdot)\) is how we weight each observation \(t\). We usually default to a triangular kernel (linearly decreases weight as distance to \(c\) increases).

\(h\) is the bandwidth - how much data around \(X_t = c\) to consider in our model. \(h\) is the most important parameter. The figure below shows how changing cutoffs changes our results:

When \(h\) is larger, bias increases, but variance decreases. When \(h\) is smaller, bias decreases, but variance increases. This is because we ideally want to only have points very close to cutoff \(c\), but limiting your observations increases variance.

Cattaneo et al (2020) have proposed a optimal bandwidth formula that minimises the Mean Squared Error, which is Bias plus Variance. The standard errors are an issue, so there are undersmoothing and robust bias correction methods.

We can show robustness of our results by just reporting different estimates from different choices of bandwidth \(h\).

We can also assume \(\pt\) and \(\pc\) take some functional form, for example - linear:

For linear models with different slopes, we estimate the regression:

\[ Y_t = \gamma + \tau D_t + \alpha X_t + \beta(X_tD_t) \]

late <- fixest::feols(Y ~ D*X, data = my_data, se = "hetero")

summary(late)One concern is that there is manipulation around the threshold \(X_t = c\). For example, welfare programmes might have a maximum income cutoff, so individuals will intentionally forgo job opportunities to select into treatment. McCray (2008) has a density test that can be implemented:

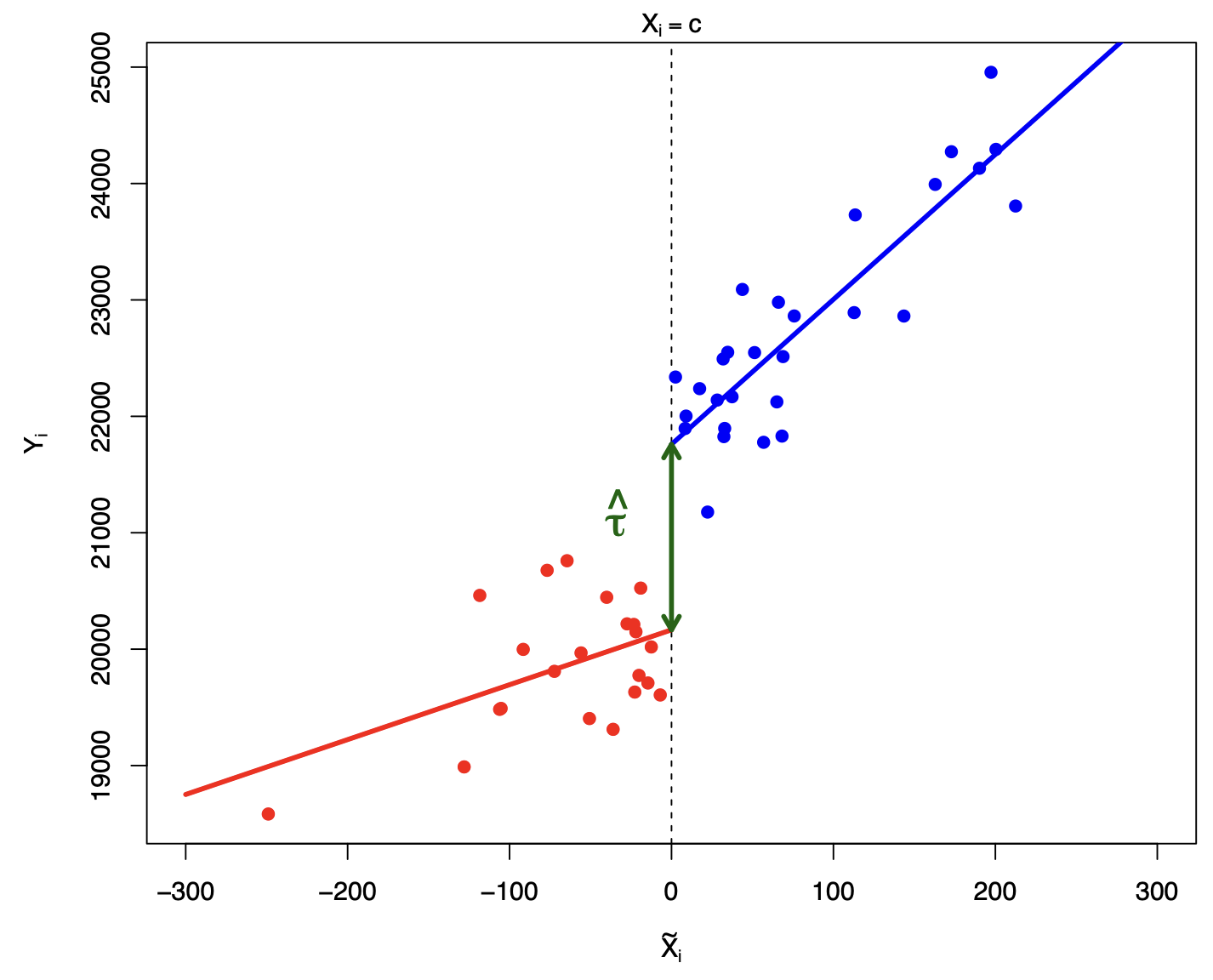

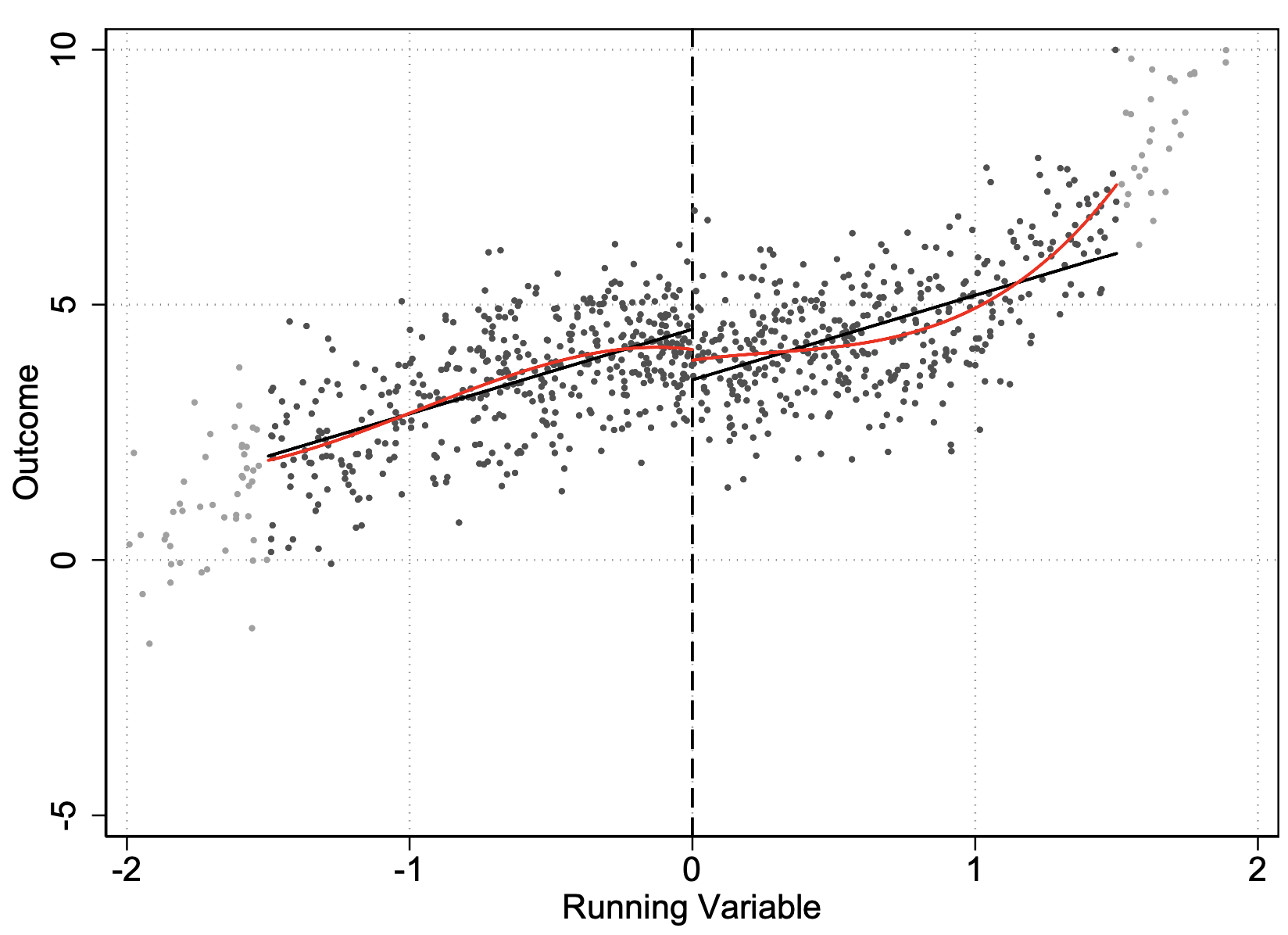

Another concern is that we might have mistakenly concluded a treatment effect, when our actual function is not plotted correct. In the figure below, we fit linear models for \(\pt\) and \(\pc\) (in black), which estimates a positive \(\tau_{LATE}\), but when visually inspecting, this is clear it is not the case:

The way to test for this is to simply visualise using rdplot:

An extension to the regression discontinuity design is the fuzzy-regression discontinuity design, when treatment is assigned based on some cutoff, but there is some non-compliance. Some people over the cutoff may on average be treated, but compliance is not perfect.

In a fuzzy regression discontinuity, we will have an encouragement variable \(Z_t\), and a treatment variable \(D_t\) that is associated with \(Z_t\). The forcing variable \(X_t\) perfectly determines encouragement \(Z_t\) at cutoff \(X_t = c\):

\[ Z_t = \begin{cases} 1 & \text{if } X_t > c \\ 0 & \text{if } X_t ≤ c \end{cases} \]

The assumptions are:

- Augmeneted Continuity: Potential outcomes \(\E(\pt, \pc | X_i = x)\) are continuous.

- Our instrumental variable assumptions of Monotonicity, exclusions restriction, and relevance of \(Z_t\) must be met.

Our estimands are the Local Intent to Treat (LITT), the effect of encouragement \(Z_t\) at the threshold:

\[ \tau_{LITT} = \E(\pt - \pc | X_i = c) \]

And the Local Average Treatment Effect (LATE) for compliers at the threshold:

\[ \tau_{LATE} = \E(\pt - \pc | X_i = c, \ \mathrm {complier}) \]

A complier is a unit \(t\) who has \(D_t = 1\) if above the cutoff \(X_t = c\), and \(D_t = 0\) if not. Note that this is only the treatment effect at the cutoff for compliers - and is not generally generalisable.

The LITT is essentially the sharp regression discontinuity of \(Z_t\) on \(Y_t\), so it is identified as:

\[ \tau_{LITT} = \lim\limits_{\epsilon \rightarrow 0^+} \E (Y_t | X_t = c + \epsilon) - \lim\limits_{\epsilon \rightarrow 0^-} \E (Y_t | X_t = c + \epsilon) \]

The LATE is the LITT for compliers (based on the IV non-compliance identification), so it is identified as:

\[ \tau_{LATE} = \frac{\tau_{LITT}}{\P(\mathrm{compliers}|X_t = c)} \]

To estimate the LATE, first we estimate the \(\tau_{LITT}\) from a sharp regression discontinuity with treatment of \(Z_t\), forcing variable \(X_t\), and outcome \(Y_t\).

Then, we can estimate the proportion of compliers at the cutoff \(X_t = c\), by running a sharp regression discontinuity with treatment of \(Z_t\), forcing variable \(X_t\), and outcome \(D_t\).

Then, we can calculate the \(\tau_{LATE}\) as:

\[ \tau_{LATE} = \frac{\tau_{LITT}}{\P(\mathrm{compliers}|X_t = c)} \]

Examiner Designs

Examiner designs are used in settings where individuals \(t\) are assigned to evaluators/examiners, who have some discretion in assigning treatment.

The classic example is judges and sentencing. We want to study the effect of incarceration on an outcome. Individuals prosecuted of a crime are first randomly assigned to courtrooms, and those courtrooms decide if these individuals will be incarcerated. However, courtrooms differ in the propensity for defendants to be incracerated. Other common set-ups include asylum decisions assigned to officers, healthcare diagnoses assigned to doctors, and so on.

More generally, we have \(n\) units, and \(K\) examiners \(1, \dots, K\) who have control over treatment status \(D_t\). Each unit \(t\) is assigned to an examiner \(k\) in a known way. The examiner \(k\) unit \(t\) is assigned to is stored in a categorical variable \(Q_t = k\).

Our assumptions for the examiner design are as follows:

- Relevance: Each examiner \(k\) should have a different propensity to assign treatment \(D\).

- Exogeneity/Ignorability: Assignment to examiners should be as-if random. There should be no backdoor paths between assignment to examiner and \(Y\).

- Exclusions Restriction: No direct relationship between assignment to examiner and \(Y\), that is not through \(D\). Exclusions restrictions can actually be allowed, as long as they occur randomly.

- Monotonicity: Examiner behaviour must be ordered. This means that if examiner \(k\) has a property, they should apply it to all subjects \(t\). For example, if \(k\) is more likely in assigning \(D\), it must be more likely for every unit \(t\) (this is an issue if an examiner has racial or gender biases for example).

If these assumptions are met, we can use two estimation methods for our instrument - which is the propensity of an examiner \(k\) assigning a treatment \(D_t = 1\).

The propensity of an examiner assigning treatment is also a time-invariant property - it does not change over time. Thus, we can use fixed effects for examiners to control for these propensities.

Thus, our instruments will be dummy variables \(Z_1, \dots, Z_{K-1}\) (The \(k-1\) is because we have to leave one category out). Any specific \(Z_k\) takes a value \(Z_{tk} = 1\) if unit \(t\) was assigned to that specific examiner \(k\), and \(Z_{tk} = 0\) if unit \(t\) was not assigned to that specific examiner \(k\).

These dummy instruments will be included in the first stage to estimate \(\hat D_t\), then in the second stage, use \(\hat D_t\) as an explanatory variable for \(Y_t\).

In R, the implementation is as follows:

fixest::feols(Y ~ 1 | D ~ as.factor(Z),

data = my_data, se = "hetero")We want to use the fact that different examiners are different - that is, variation in treatment assignment propensity to examiners. Thus, we need to estimate the latent (unobserved) propensity of each examiner \(k\).

We do this by finding the probability of being assigned to treatment \(D_t = 1\) for examiner \(k\), but ignoring unit \(t\) themselves:

\[ \hat L_t^{(k)} = \frac{\overbrace{\sum_{j≠t} \mathbb I[Q_j = Q_t]D_j}^{\text{num of treated for examiner k }}}{\underbrace{\sum_{j≠t} \mathbb I[Q_j = Q_t]}_{\text{total num assigned to examiner k}}} \]

Where \(\mathbb I[Q_j = Q_t]\) is an indicator function that only takes the value of 1 if the examiner of unit \(j\) is the same as the examiner of unit \(t\). We leave \(t\) out in the sum because you do not want to use \(D\) to measure the instrument, to avoid ignorability violations. We can estimate this in R:

my_data$L <- ave(my_data$D, my_data$Q, FUN = mean)Where D is the treatment variable, and Q is the assigned examiner variable.

We then use \(\hat L_t^{(k)}\) as an instrument for \(D_t\), and use a instrumental variables/2-stage-least-squares estimator.

fixest::feols(Y ~ 1 | D ~ L, data = my_data, se = "hetero")Differences-in-Differences

Selection on Observables

There are two assumptions for selection on observables:

Conditional Ignorability (also called conditional independence) means that among units \(i\) with identical confounder values \(\mathcal X_i\), treatment \(D_i\) is as-if randomly assigned. Potential outcomes are independent from treatment within each specific confounder value \(\mathcal X_i = x\).

\[ (\pc, \pt) \ind D_t \ | \ \set X_t = x, \ \forall \ x \in \set X \]

This assumption implies that given any value of confounders \(\set X_t = x\), potential outcomes are equivalent between treatment and control groups:

\[ \begin{align} & \E(\pc|D_t = 1, \set X_t = x) \ = \ \E(\pc|D_t = 0, \set X_t = x) \ = \ \E(\pc|\set X_t = x) \\ & \E(\pt|D_t = 1, \set X_t = x) \ = \ \E(\pt|D_t = 0, \set X_t = x) \ = \ \E(\pt|\set X_t = x) \end{align} \tag{12.1}\]

Common Support is the second assumption, and it states for any unit \(t\) with any value of \(\mathcal X_t\), they have a non-zero probability they can be assigned to both control and treatment.

A few tips for selection controls in set \(\set X\):

- Good controls are confounders \(X\) who cause \(D\) (i.e. \(X \rightarrow D\)), and are associated with \(Y\). We want to control for all of these.

- Bad controls include any variable that is caused by \(D\), i.e. \(D \rightarrow W\). We do not need to control for this because \(W\) isn’t causing selection into \(D\), it is actually itself caused by \(D\). Another bad control is a variable \(Z\) that only causes \(D\), and not \(Y\). This reduces the variation in \(D\), which may amplify any other confounders unaccounted for.

- Neutral controls are variables that only cause \(Y\) and are not associated with \(D\). They do not affect the causal identification, but can reduce our standard errors.

Using these assumptions, we can first identify the CATE, which will allow us to identify the ATE. Let us first start with the definition of CATE (definition 5.6):

\[ \begin{align} \tau_{CATE}(x) & = \E(\pt - \pc \ | \ \set X_t = x) \\ & = \E(\pt | \set X_t = x) - \E(\pc|\set X_t = x) \\ \end{align} \]

Now, from the properties implied by conditional ignorability given in eq. 12.1, we get

\[ \begin{align} \tau_{CATE}(x) & = \E(\pt|D_i = 1, \set X_t = x) - \E(\pc|D_i = 0, \set X_t = x) \\ & = \E(Y_{t}|D_t = 1, \mathcal X_t = x) - \E(Y_{t}|D_t = 0, \set X_t = x) \\ \end{align} \]

And the second step above is because \(\pt|D_i = 1\) and \(\pc|D_i = 0\) are observable outcomes (definition 5.7). Thus, with independence, we can identify the CATE with just observed outcomes.

Let us consider the definition of the ATE, which is \(\E(\pt - \pc)\). From the definition of expectation given in definition 1.2, we can rewrite the ATE as

\[ \tau_{ATE} = \int\tau_{CATE}(x) \P(\mathcal x) dy \]

Which is a weighted average. We established above that we can identify the CATE. Thus, we can plug the CATE into the ATE to get our identified ATE:

\[ \tau_{ATE} = \int [\E(Y_{t}|D_t = 1, \set X_t = x) - \E(Y_{t}|D_t = 0, \set X_t = x)] \P(x) dy \]

And all the values in this equation are observed outcomes \(Y_t\), meaning if we control for set of confounders \(\mathcal X\), our correlation becomes a causal effect.

Using these assumptions, we can first identify the CATE, which will allow us to identify the ATT. Let us first start with the definition of CATE (definition 5.6):

\[ \begin{align} \tau_{CATE}(x) & = \E(\pt - \pc \ | \ \set X_t = x) \\ & = \E(\pt | \set X_t = x) - \E(\pc|\set X_t = x) \\ \end{align} \]

Now, from the properties implied by conditional ignorability given in eq. 12.1, we get

\[ \begin{align} \tau_{CATE}(x) & = \E(\pt|D_i = 1, \set X_t = x) - \E(\pc|D_i = 0, \set X_t = x) \\ & = \E(Y_{t}|D_t = 1, \mathcal X_t = x) - \E(Y_{t}|D_t = 0, \set X_t = x) \\ \end{align} \]

And the second step above is because \(\pt|D_i = 1\) and \(\pc|D_i = 0\) are observable outcomes (definition 5.7). Thus, with independence, we can identify the CATE with just observed outcomes.

Let us consider the definition of the ATT, which is \(\E(\pc = \pt | D_i = 1)\). From the definition expectation given in definition 1.2, we can rewrite the ATT as

\[ \tau_{ATT} = \int \tau_{CATE}(x) \P(x|D_t = 1) dy \]

Which is a weighted average. We established above that we can identify the CATE. Thus, we can plug CATE into the ATE to get our identified ATT:

\[ \tau_{ATT} = \int [\E(Y_{t}|D_t = 1, \set X_t = x) - \E(Y_{t}|D_t = 0, \mathcal X_t = x)] \P(x|D_t = 1) dy \]

And all the values in this equation are observed outcomes \(Y_t\), meaning if we control for set of confounders \(\mathcal X\), our correlation becomes a causal effect.

Assuming we meet the assumptions, there are multiple estimators, including regression, matching, propensity score matching, and weighting.

Regression is the most popular estimator for selection on observables. There are two types of regression estimators.

Classical linear regression with OLS and robust standard errors is used to estimate the ATE when we believe we have constant treatment effects for all units (where each unit \(t\) has the same \(\tau\) effect):

\[ \textcolor{purple}{Y_t^{(d)}} = \alpha + D_t\tau + \b x_t \b\gamma + \eps_t \]

ate <- fixest::feols(Y ~ D + X1 + X2 + X3,

data = mydata, se = "hetero")

summary(ate)However, classical linear regression is biased for the ATE if we have heterogenous treatment effects (different units have different \(\tau\)). It actually is an unbiased estimator for a weighted average of the ATT and ATU, not the ATE.

Instead, with heterogeneity, we should use the Fully Interacted Estimator:

\[ \textcolor{purple}{Y_t^{(d)}} = \alpha + D_t \tau + (\b x_t - \bar{\b x})\b\beta + D_t(\b x_t - \bar{\b x})\b\gamma + \eps_t \]

ate <- estimatr::lm_lin(Y ~ D, covariates = ~ X1 + X2 + X3,

data = my_data)

summary(ate)The fully interacted estimator is slightly biased when estimating \(\tau_{ATE}\), but the bias is arbitrarily small in large sample sizes. When we have a good amount of data, we tend to default to this estimator.

Matching estimates missing potential outcomes/counterfactuals for each observation in the treated group, by matching an untreated observation to that treated observation. The matching process is done by similarity on covariates \(\set X\). Matching estimates the ATT:

\[ \hat\tau_{ATT} = \frac{1}{N_1} \sum\limits_{t:D_i = 1}^{N_1}(Y_t - \tilde Y_t) \]

Where \(N_1\) is the number of observations of units in the treatment group, \(Y_i\) is the observed \(Y\) of unit \(t\) in the treated group, and \(\tilde Y_i\) is the observed \(Y\) value of the control unit matched to unit \(t\). Matching takes an average difference of the matched pairs.

We can also match multiple control units \(\tilde Y_t\) to one treated unit \(t\), and average the value of those control units to create a closer match with the treated unit \(t\).

To determine what units are “closest” to each other in similarity of covariates \(\set X\) for matching, the typical choice is mahalanobis distance, which calculates the distance between a unit \(i\) and \(j\):

\[ D_M(i,j) = \sqrt{(\b x_i - \b x_j)^\top \b\Sigma_x^{-1}(\b x_i - \b x_j)} \]

Where \(\b\Sigma_x\) is the covariance matrix of confounders \(\set X\). The units in treatment and control that have the smallest distances are matched. Matching is done in R:

#matching units

match_obj <- MatchIt::matchit(D ~ X1 + X2 + X3, data = my_data,

method = "nearest", distance = "mahalanobis")

match_data <- MatchIt::match.data(match_obj, weights = "nn_weights")

#estimate

att <- estimatr::lm_robust(Y ~ D, data = match_data, weights = nn_weights)

summary(att)The matching estimator is prone to bias/poor-matches as the number of covariates you have increases. Generally, with many covaraites, propensity scores are more popular.

Propensity score matching is similar to matching, and also estimates the ATT.

However, instead of matching on covariates, it matches on the likelihood of a unit \(t\) receiving treatment \(D_t = 1\), based on their covariate \(\set X_t\) values. This likelihood/probability is called the propensity score.

\[ \pr_t(\set X_t) = \P(D_t = 1 | \set X_t) \]

However, we do not actually observe \(\pr_t(\set X_t)\). We can estimate \(\pr_t(\set X_t)\) with a binary response model with outcome \(D_t\), and explanatory variables \(\set X\). Then using the fitted probabilities \(\P(D_t = 1) = \hat\pr_t(\set X_t)\), we can conduct matching based on these estimates.

To implement propensity score matching in R, we start with our binary response variable. The most common choice is logistic regression, but random forest is also possible:

# logistic model

ps_model <- glm(D ~ X1 + X2, data = my_data, family = "binomial")

# rf model

ps_model <- randomForest::randomForest(D ~ X1 + X2,

data = my_data,

na.action = na.omit)

# estimate propensity scores

my_data$ps <- predict(ps_model, type = "response")Then, we conduct matching with the estimated propensity scores:

#matching units

match_obj <- MatchIt::matchit(D ~ ps, data = my_data,

method = "nearest", distance = "mahalanobis")

match_data <- MatchIt::match.data(match_obj, weights = "pscore_weights")

#estimate

att <- estimatr::lm_robust(Y ~ D, data = match_data,

weights = pscore_weights)

summary(att)Matching only recovers the ATT. However, if we want the ATE, we can use propensity scores in a inverse probability weighting (IPW) estimator. It can be shown with math that the ATE with propensity scores \(\pr_t(\set X_t)\) can be identified as:

\[ \tau_{ATE} = \E\left[ Y_t \cdot \frac{D_t - \pr_t(\set X_t)}{\pr_t(\set X_t)(1-\pr_t(\set X_t))} \right] \]

We can use our sample equivalents to estimate the ATE:

\[ \begin{align} \hat\tau_{ATE} & = \frac{1}{N}\sum\limits_{i=1}^N\left(Y_t \cdot \frac{D_t - \hat\pr_t(\set X_t)}{\hat\pr_t(\set X_t)(1-\hat\pr_t(\set X_t))} \right) \\ & = \frac{1}{N} \sum\limits_{i=1}^N\left( Y_tD_t\frac{1}{\hat\pr_t(\set X_t)} - Y_t(1-D_t)\frac{1}{1 - \hat\pr_t(\set X_t)}\right) \end{align} \]

We see that units who are unlikely to recieve treatment (low propensity scores) that actually get treated get weighted more, and units who are likely to be treated (high propensity scores) but don’t get treated also get weighted more.

We first estimate the propensity scores with either logistic or random forest:

# logistic model

ps_model <- glm(D ~ X1 + X2, data = my_data, family = "binomial")

# rf model

ps_model <- randomForest::randomForest(D ~ X1 + X2,

data = my_data,

na.action = na.omit)

# estimate propensity scores

my_data$ps <- predict(ps_model, type = "response")Then, we calculate the weights and estimate:

my_data$ipw <- ifelse(mydata$D == 1, 1/my_data$ps, 1/(1-my_data$ps))

ate <- estimatr::lm_robust(Y~D, data = my_data, weights = ipw)The IPW estimator is asymptotically consistent, but has poor small sample properties, and are sensitive to extreme values of \(\hat\pr_t(\set X_t)\).

We should generally be careful with selection on observables, as it is considered to be the least robust of the quasi-experimental designs. This is particularly the case in the social sciences, when there are tons and tons of unobservable confounders which are nearly impossible to control for.